As of December 31, 2025

Cobalt by Hamilton Lane (Cobalt) gives GPs access to deep market analysis, transparent data and LP-grade due diligence tools – providing a clearer view of both their funds’ and competitors’ performance.

Our global data ecosystem is built on decades of investing experience, seamlessly bringing together cutting-edge tools, human expertise and proprietary insight.

access within one platform:

Market Research and Thought Leadership Powered by HL Data

& Insights

Due Diligence Workflow to Explore Your Data Through the LP Lens

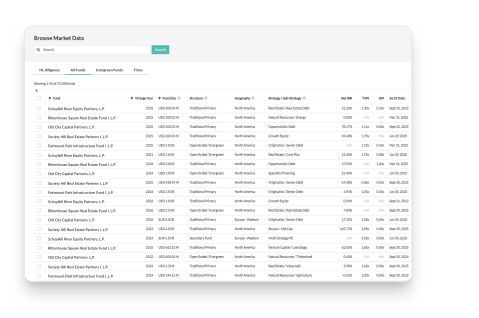

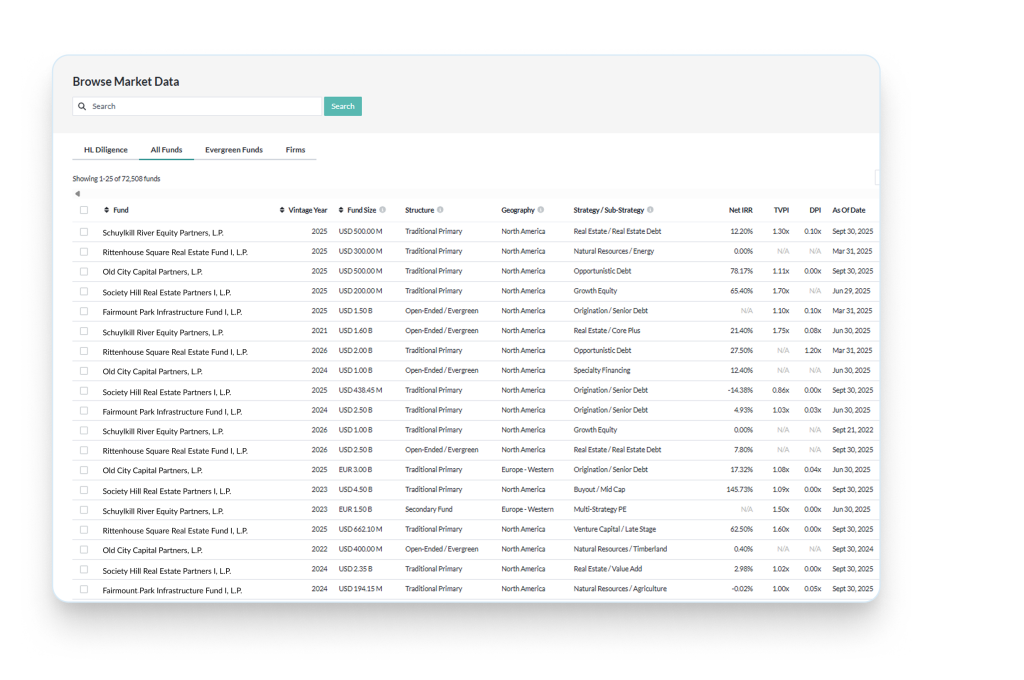

HL Fund Database with Transparent Net Return Data

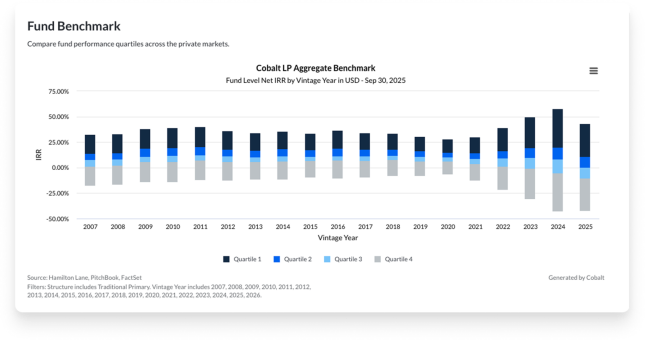

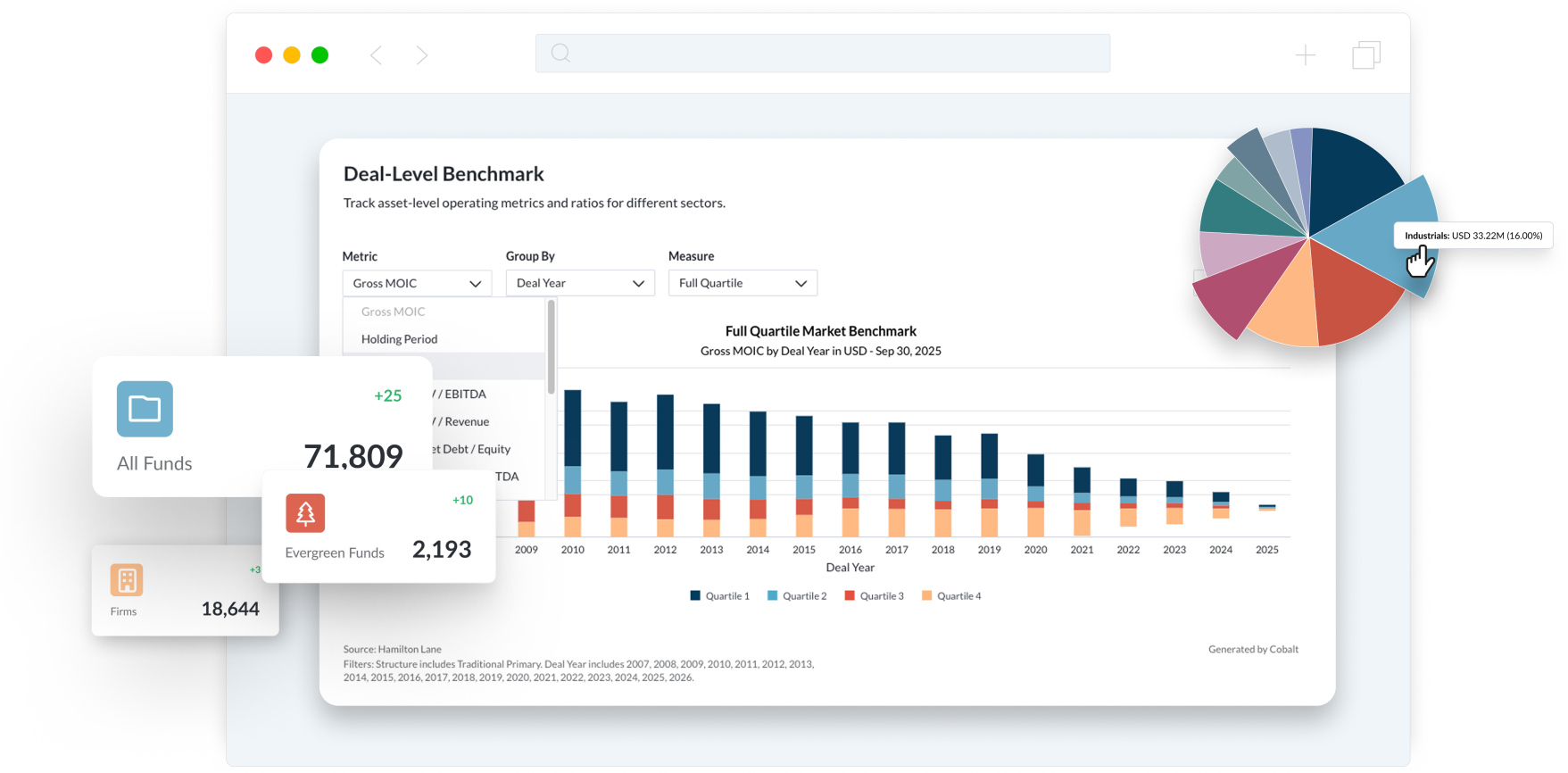

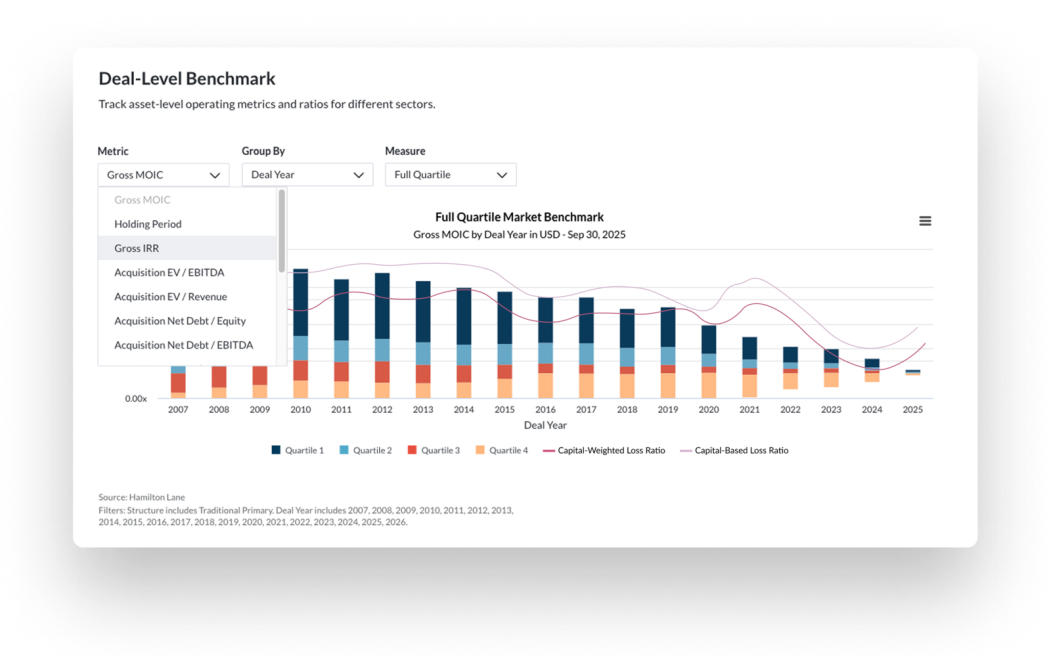

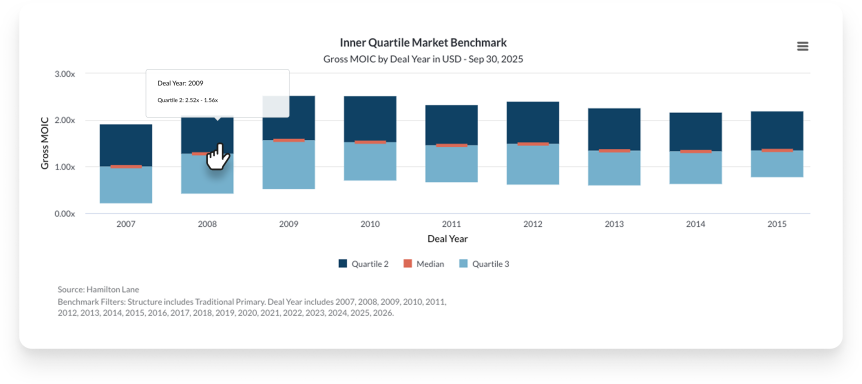

Fund‑ and Deal‑Level Benchmarking with Custom Capabilities

Book a Demo

Connect with us to see our technology and insights

in action

DISCLOSURES

As of December 31, 2025 unless otherwise noted.

This has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients are requested to maintain the confidentiality of the information contained herein. This may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane. The information contained may include forward-looking statements regarding returns, performance, opinions, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgement, which may change in the future. The information included has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable, but the accuracy of such information cannot be guaranteed. The information herein is not intended to provide, and should not be relied upon for accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

This presentation has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane.

Accordingly, the recipients of this presentation are requested to maintain the confidentiality of the information contained herein. This presentation may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts of future performance or other events contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. Past performance of the investments described herein is not indicative of future results. In addition, nothing contained herein shall be deemed to be a prediction of future performance. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable, but the accuracy of such information cannot be guaranteed. This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

Certain of the performance results included herein do not reflect the deduction of any applicable advisory or management fees, since it is not possible to allocate such fees accurately Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorised and regulated by the Financial Conduct Authority

(FCA). In the United Kingdom this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services licence under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private Assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our websitewww.hamiltonlane.com.au.

Any tables, graphs or charts relating to past performance included in this presentation are intended only to illustrate the performance of the indices, composites, specific accounts or funds referred to for the historical periods shown. Such tables, graphs and charts are not intended to predict future performance and should not be used as the basis for an investment decision.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your

accounting, legal, tax or other advisors about the matters discussed herein. The calculations contained in this document are made by Hamilton Lane based on information provided by the general partner (e.g. cash flows and valuations), and have not been prepared, reviewed or approved by the general partners.

This material is being issued by Hamilton Lane (UK) Limited (DIFC Branch) (“Hamilton Lane DIFC”). Hamilton Lane DIFC is regulated by the Dubai Financial Services Authority (“DFSA”).

This document is intended for Professional Clients and Market Counterparties only as defined by the DFSA and no other person should act upon it.

In some instances, this presentation may be distributed by MPW Capital Advisors Limited (“MPW”) on behalf of Hamilton Lane and is for informational purposes only. MPW is

incorporated in the Abu Dhabi Global Market (“ADGM”) and is authorized and regulated by the Financial Services Regulatory Authority (“FSRA”)”. Nothing contained in this presentation constitutes investment, legal or tax advice. Neither the information, nor any opinion contained in this presentation constitutes a solicitation or offer by MPW, to buy or sell any securities or other financial instruments or products. Decisions based on information contained on this presentation are the sole responsibility of the visitor. No guarantee, representation, undertaking, warranty, advice or opinion, express or implied, is given by MPW or their respective directors, officers, partners, shareholders or members or employees or agents as to the accuracy, authenticity or completeness of the information or opinions contained on this presentation and no liability is accepted by such persons for the accuracy, authenticity or completeness of any such information or opinions. Important risk factors that could impact our ability to deliver the services include, among others, the following: developments and changes in laws and regulations, including increased regulation of the financial services industry through legislative action and revised rules and standards applied by regulators.

Furthermore, any opinions are subject to change and may be superseded without notice.

This presentation is intended only for Professional Clients or Market Counterparties (as defined by the Financial Services Regulatory Authority) and no other Person should act upon it.

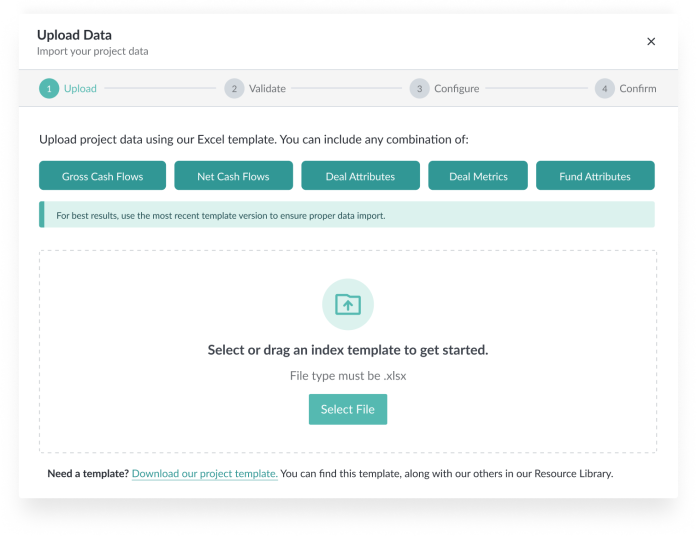

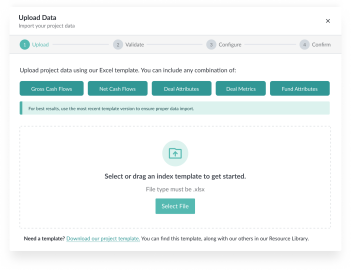

Upload your fund data to Cobalt and evaluate your performance as an LP would.

Ask us about easily sharing your data with the HL Investment Team

Hamilton Lane’s

Proprietary Analytics

Benchmark your funds and deals against the HL dataset

Uplevel your analysis with an

LP-grade view of your own funds

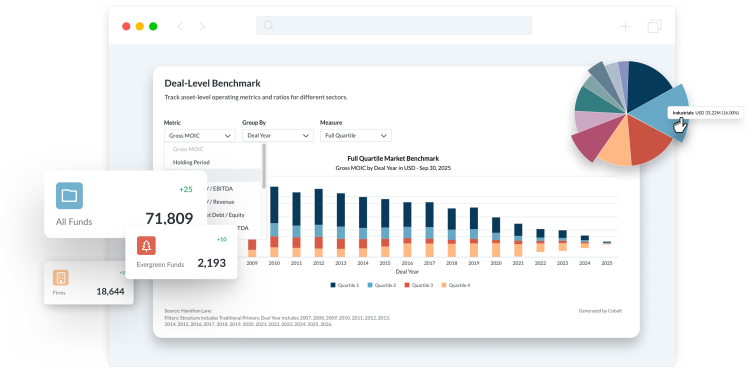

Your Fund

and Deal Data

Secure, encrypted environment — your uploaded data stays private by default

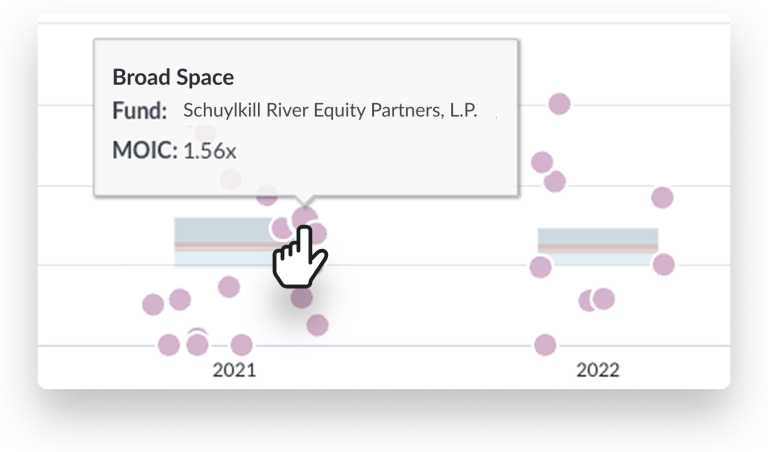

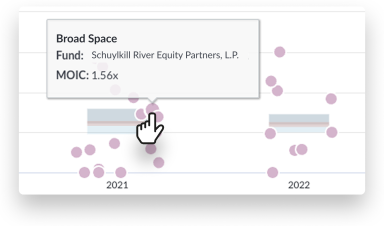

See how your fund strategies compare to your peer set and easily track performance versus competitors over time.

PME & Cash Flow

Analytics

Conduct public market equivalent (PME) and cash flow analytics

View value drivers across metrics and compare cash flow pacing to the market

Custom Benchmarks

& Target Lists

Select your preferred set of peer funds to build benchmarks tailored to your strategy

Monitor peer activity, including new funds to market and fund performance

Competitive

Landscape

Access net performance data on your own funds alongside the broader market

Filter by strategy, vintage, geography and sector

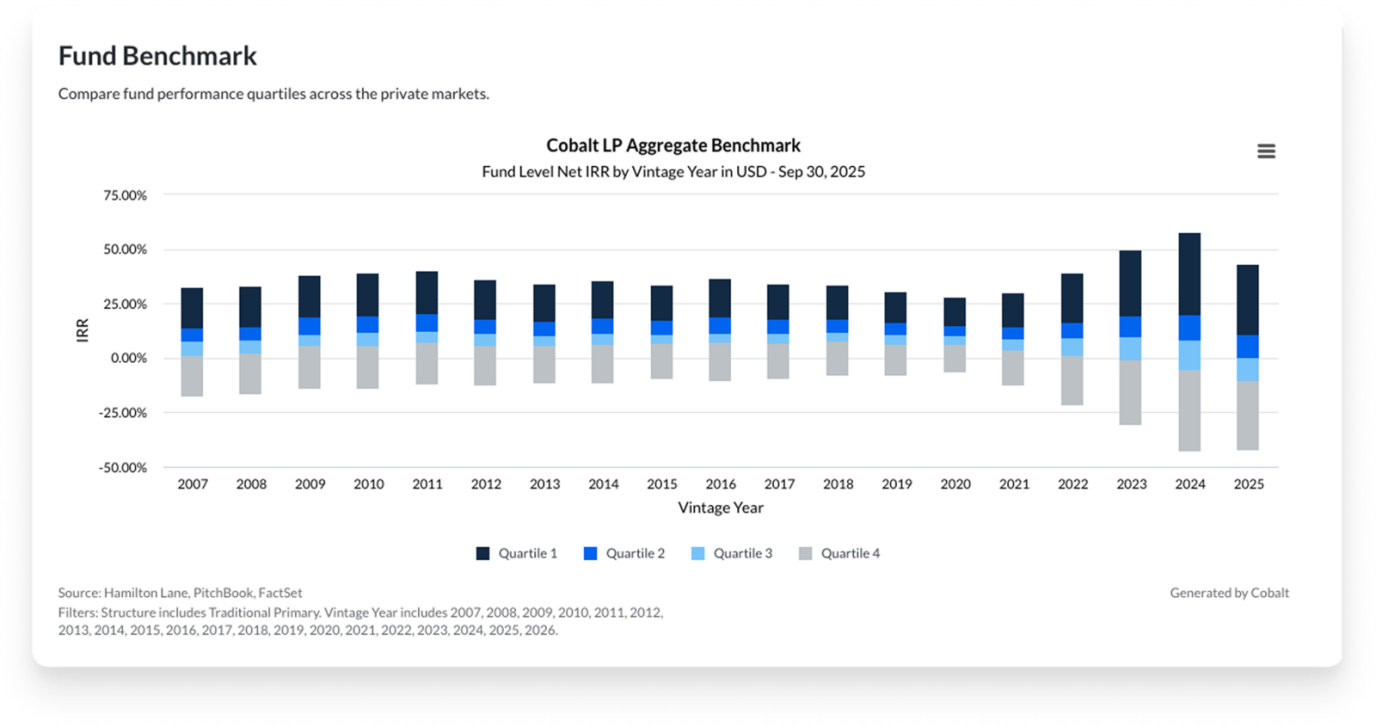

More than 34 years of direct industry and investing experience reflected in our benchmarks.

Industry Trend

Analysis

Fundraising trends, contribution & distribution pacing, and cash flow tracking

Access Hamilton Lane’s proprietary research, including valuation estimates, GP term benchmarks and the annual HL Market Overview

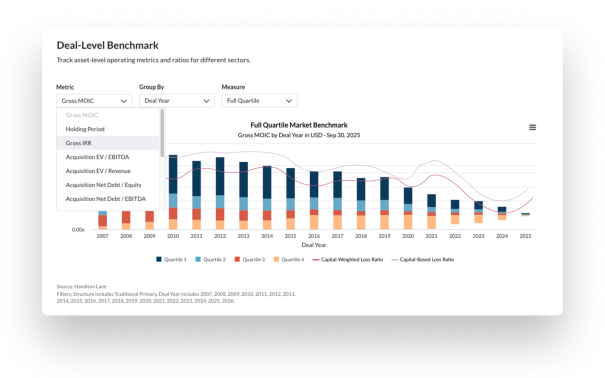

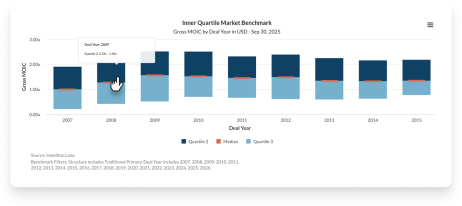

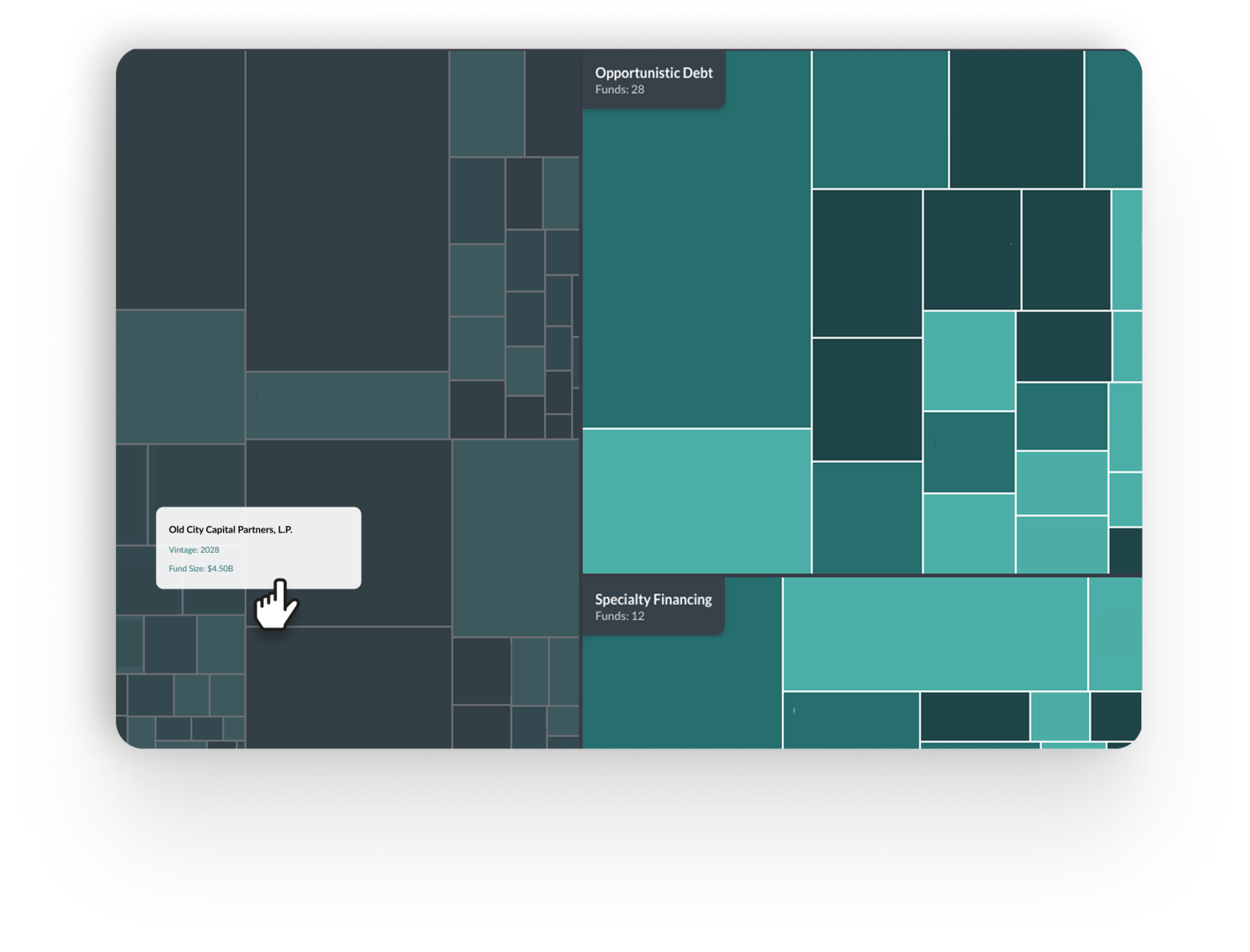

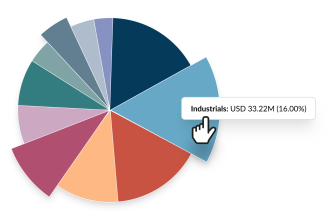

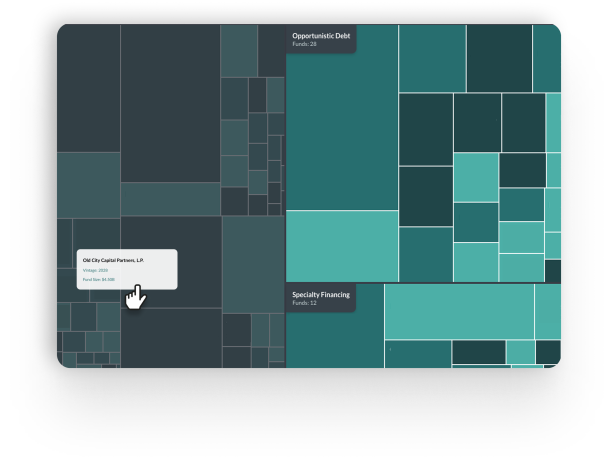

Deeper Deal-Level Visibility

Coverage of 180,000+ portfolio companies, coupled with available deal-level MOIC and operating metrics (as of 12/31/25)

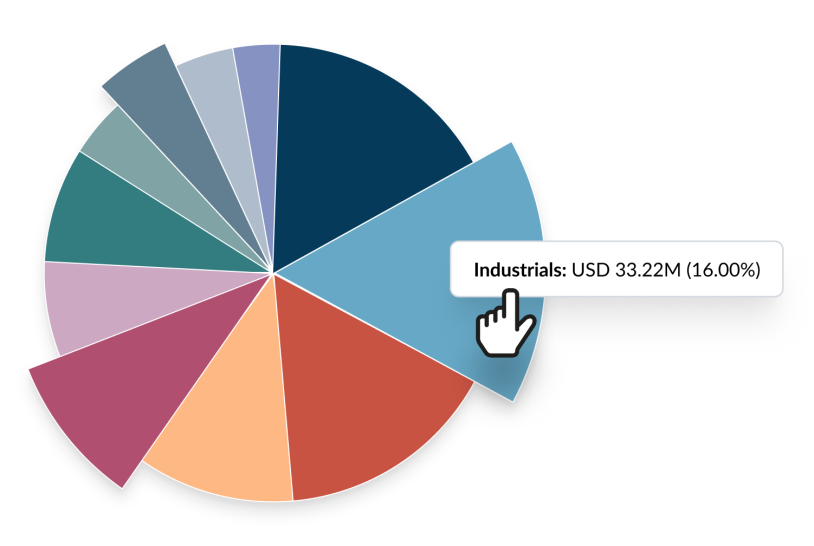

Breakdowns by loss ratios, sector performance, geography, entry & exit multiples

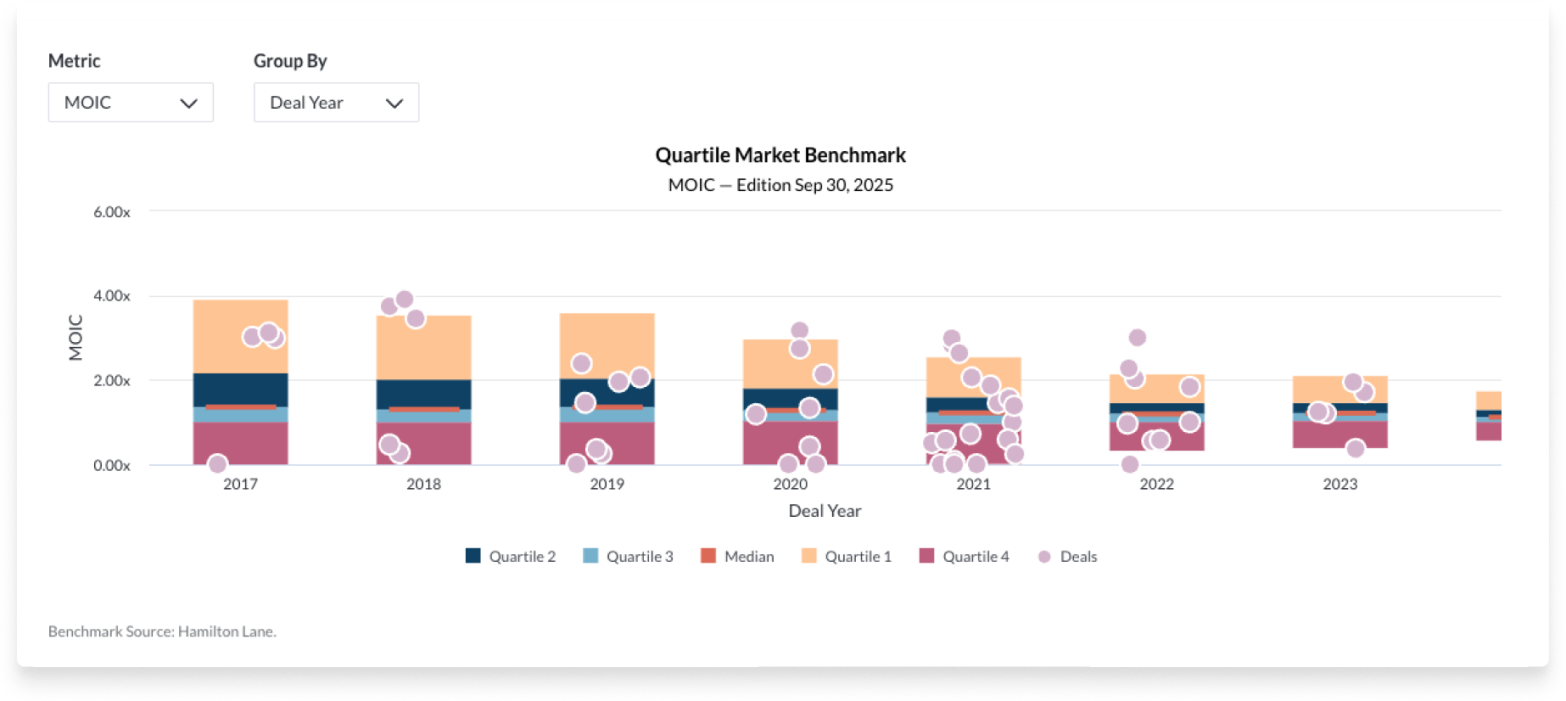

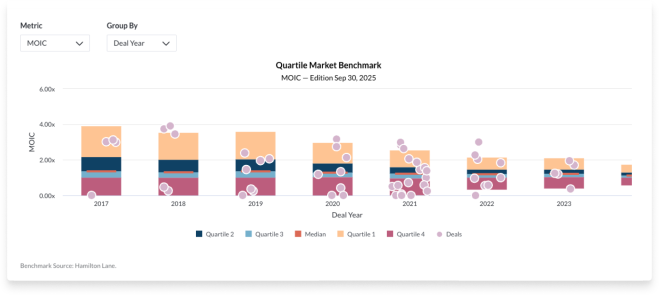

Transparent, High-Quality Benchmarks

Minimal survivorship bias with transparent, in-depth benchmark construction

Full constituent-level visibility — view the underlying funds that make up a benchmark

Analyze j-curves and evaluate risk and returns across asset classes, strategies and geographies

As of December 31, 2025

Market Research and Thought Leadership Powered by HL Data

& Insights

Due Diligence Workflow to Explore Your Data Through the LP Lens

HL Fund Database with Transparent Net Return Data

Fund‑ and Deal‑Level Benchmarking with Custom Capabilities

access within one platform:

Cobalt by Hamilton Lane (Cobalt) gives GPs access to deep market analysis, transparent data and LP-grade due diligence tools – providing a clearer view of both their funds’ and competitors’ performance.

Our global data ecosystem is built on decades of investing experience, seamlessly bringing together cutting-edge tools, human expertise and proprietary insight.

& Analytics

HAMILTONLANE.COM

Book a Demo

Connect with us to see our technology and insights in action

Upload your fund data to Cobalt and evaluate your performance as an LP would.

Your Fund and Deal Data

Secure, encrypted environment — your uploaded data stays private by default

Hamilton Lane’s Proprietary Analytics

Benchmark your funds and deals against the HL dataset

Uplevel your analysis with an LP-grade view of your own funds

Ask us about easily sharing your data with the HL Investment Team

DISCLOSURES

As of December 31, 2025 unless otherwise noted.

This presentation has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this presentation are requested to maintain the confidentiality of the information contained herein. This presentation may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgement, which may change in the future.

KEY RISKS

Investors considering an investment in the Fund should be aware of potential risks, some of which are summarised below. This presentation does not purport to be a complete disclosure of all risks that may be relevant to a decision to invest in the Fund. Prospective investors must rely upon their own examination of, and ability to understand, the nature of this investment, including the risks involved, in making a decision to invest in the Fund. There can be no assurance that the Fund will be able to achieve its investment objective or that investors will recoup a return of their capital. The Fund involves speculative and illiquid securities involving substantial risk of loss; investors can lose their investment in whole or in part.

An investment in the Fund is appropriate only for those investors who do not require a liquid investment, for whom an investment in the Fund does not constitute a complete investment programme, and who fully understand and can assume the risks of an investment in the Fund.

Limited Operating History

The Fund may have limited operating history upon which to evaluate its likely performance. Past performance of other funds and accounts managed or advised by Hamilton Lane is not a reliable indicator of future performance of the Fund.

Identification and Availability of Investment Opportunities; No Assurance of Investment Return

There can be no assurance that the Fund will be able to identify sufficient, attractive investment opportunities to meet its investment objectives, or that it will otherwise be successful in implementing its investment objectives or avoiding losses (up to and including the loss of the entire amount invested).

Illiquidity

The Fund will invest a significant portion of its assets in highly illiquid investments and does not expect to be able to transfer its investments in, or to withdraw from, such investments. There is no current public trading market for interests in the Fund, and investors should expect their investment to be illiquid for the duration of their holding. Where the Fund offers redemption facilities, the Fund may suspend or cap redemptions and should a large number of investors seek to exit, the Fund could be forced to liquidate investments prematurely, causing losses.

Performance may differ between investors

Performance for individual investors may vary from the Fund's overall performance because of the timing of an investor's admission to the Fund, the class or series in which they invest (including because of different fee structures or currency fluctuations), and the timing and way capital is deployed and returned.

Valuation Methodology Risks

The valuation methodologies used to value certain of the Fund's investments may change over time and have subjective elements. Valuations are subject to determinations, judgements, opinions, and will, in certain circumstances, not be accurate, and other third parties or investors may disagree with such valuations. Valuation methodologies will also involve assumptions and opinions about future events, which may or may not turn out to be correct.

Performance Data

Total performance includes both realised and unrealised investments. Unrealised investment values are prepared by third-party valuation providers and reviewed by Hamilton Lane; actual realised returns may differ materially from these estimated values due to market conditions, transaction costs, and timing of disposition. Where gross performance data is used, such data does not include fees, expenses and carried interest, and investors should be aware that net performance will be significantly lower. Past performance is not a reliable indicator of future performance.

In view of the risks noted above, the Fund should be considered a speculative investment and prospective investors should invest in the Fund only if they can sustain a complete loss of their investment.

Please refer to the Private Placement Memorandum/Prospectus for further information on the risks involved with investing in this product.

Transparent, High-Quality Benchmarks

Minimal survivorship bias with transparent, in-depth benchmark construction

Full constituent-level visibility — view the underlying funds that make up a benchmark

Analyze j-curves and evaluate risk and returns across asset classes, strategies and geographies

More than 34 years of direct industry and investing experience reflected in our benchmarks.

Deeper Deal-Level Visibility

Coverage of 180,000+ portfolio companies, coupled with available deal-level MOIC and operating metrics (as of 12/31/25)

Breakdowns by loss ratios, sector performance, geography, entry & exit multiples

Industry Trend Analysis

Fundraising trends, contribution & distribution pacing, and cash flow tracking

Access Hamilton Lane’s proprietary research, including valuation estimates, GP term benchmarks and the annual HL Market Overview

Custom Benchmarks & Target Lists

Select your preferred set of peer funds to build benchmarks tailored to your strategy

Monitor peer activity, including new funds to market and fund performance

Competitive Landscape

Access net performance data on your own funds alongside the broader market

Filter by strategy, vintage, geography and sector

See how your fund strategies compare to your peer set and easily track performance versus competitors over time.

PME & Cash Flow Analytics

Conduct public market equivalent (PME) and cash flow analytics

View value drivers across metrics and compare cash flow pacing to the market